Flood Insurance Claims: A Fat Tail Getting Fatter

Floods remain some of the worst disasters around the world. They cause more property damage and insured losses than many other types of events. In the US, floods are primarily insured through the federally-run National Flood Insurance Program (NFIP). This program has been making the headlines recently as Congress tries to address the program’s massive debt from Hurricanes Katrina, Ike, and Sandy; homeowners bemoan high flood insurance costs; communities receive new flood maps suggesting flood risk has changed over time; and disaster victims wonder how to rebuild to prevent future losses and keep insurance costs manageable.

We have been examining the distribution of NFIP claims, provided by the Federal Emergency Management Agency to the Wharton Risk Center. Individual claims are aggregated to census tracts and months, over the years 1978 to 2012. We find that this distribution is decidedly fat-tailed. This means that yearly losses can be hopelessly volatile and, as such, historical averages are not good predictors of future losses. For those more technically inclined, we have been doing this by fitting a Pareto distribution to the aggregate claims. Our estimation of the tail index gives an indication of the fatness of the tail. The smaller the tail index, the fatter the tail.

That flood claims are fat-tailed is, in and of itself, not so surprising. Many disaster losses have been found to exhibit fat tails. What is concerning, however, is that the tail of flood insurance claims seems to be getting fatter over the time period in our data. This would indicate the extremes are getting even more extreme. One way to examine this is to use the so-called Hill estimator, which gives an estimate of the tail index (here, based on the largest 10% of claims), for each year. When we plot estimates of the tail index using this method, there is a clear downward trend, as seen in the figure below. Lower values, fatter tail. The blue diamonds are the yearly estimates and the black line is a fitted linear trend line to those estimates.

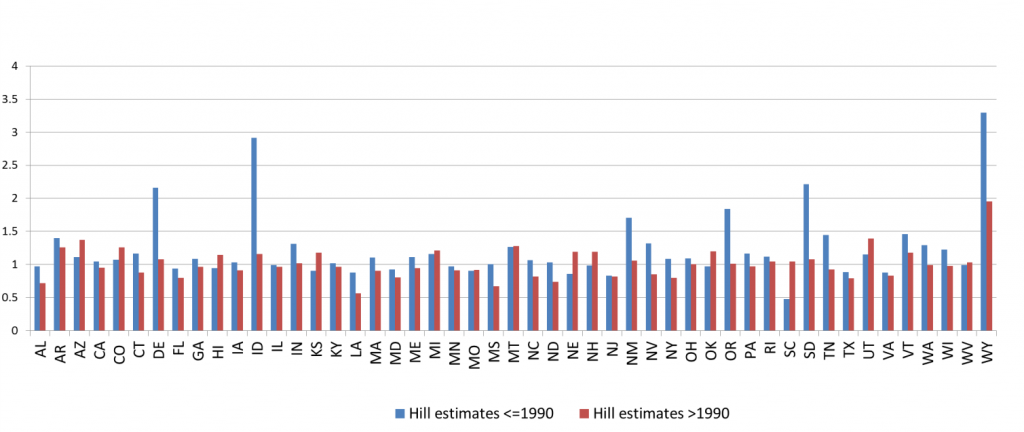

We also looked at the tail index by state. We broke the data into two periods, 1978-1990 and 1990-2012, and estimated the tail index (using maximum likelihood) for each period for each state in the country. For all but a handful, the tail index is lower in the later period, indicating that the tail of the distribution of flood claims is fatter in the later period.

We cannot yet untangle what is driving this change in the distribution. Is it caused by changes in economic activity, more development in high-risk areas, changes in the composition of the NFIP, or climate-induced changes in the frequency or severity of flooding? Most likely some mix of all of these factors. What we do know is that if the tails of the distribution keep getting fatter (and particularly if these changes in insured losses mirror similar changes in total, society-wide damages), we may need to rethink our risk management strategies. Lower tail indices mean even more devastating flood disasters will come. New records will soon be set.

About Carolyn Kousky

Carolyn Kousky is a fellow at Resources for the Future. Her research focuses on natural resource management, decisionmaking under uncertainty, and individual and societal responses to natural disaster risk.

- Web |

- More Posts (9)

About Erwann Michel-Kerjan

Dr. Erwann Michel-Kerjan is an authority on managing the risks, financial impacts, and public policy challenges associated with catastrophic events. He is currently managing director of the Risk Management and Decision Processes Center at the University of Pennsylvania’s Wharton Business School.

- Web |

- More Posts (1)

About Roger Cooke

Roger Cooke is a senior fellow and the first appointee to the Chauncey Starr Chair in Risk Analysis at Resources for the Future.

- Web |

- More Posts (5)

Subscribe; to our RSS Feed

Subscribe; to our RSS Feed

Comments

One Response to “Flood Insurance Claims: A Fat Tail Getting Fatter”Trackbacks

Check out what others are saying...[…] the National Flood Insurance Program—and it seems that extreme events and damage are becoming “even more extreme,” according to RFF’s Roger Cooke, Carolyn Kousky, and colleague Erwann Michel-Kerjan of the […]